TL;DR

- The 2026 crypto banking landscape splits into four categories: institutional crypto banks (Sygnum, AMINA, Anchorage), retail crypto-friendly neobanks (Revolut, Cash App, Robinhood), pure crypto neobanks (Juno, Bleap), and infrastructure-led stablecoin banks (Karsa, Mode, and the new tokenized-deposit issuers).

- The right choice for a user depends on jurisdiction, regulatory protection, asset coverage, and whether they need fiat rails, on-chain rails, or both.

- For marketing leaders launching a crypto neobank, the consistent lesson from the leaders is that positioning and community come before product features.

- Stablecoin neobanks are the fastest-growing subcategory; expect them to outpace general crypto banks through 2027.

- AI-led discovery (ChatGPT, Perplexity, AI Overviews) is already a meaningful acquisition channel for crypto banks, yet most ignore it.

What is a crypto bank?

A crypto bank is a regulated banking institution or banking-licensed digital platform that lets users hold, transact, earn yield on, and integrate cryptocurrencies and stablecoins alongside traditional fiat. The category includes full-license Swiss and US institutional crypto banks, hybrid neobanks that added crypto, and Web3-native banking products built on stablecoin rails.

A crypto bank differs from a crypto exchange in three ways: it holds a banking license or partners with one, it offers payment rails including IBAN and SWIFT, and it provides FDIC, SIPC, or equivalent protection on fiat balances. A wallet is custody; an exchange is trading; a crypto bank is a regulated banking relationship with digital asset capability built in.

The 4 categories of crypto bank in 2026

Category 1: Institutional crypto banks

Full-license banks focused on institutional and high-net-worth clients. Custody, lending, structured products, prime services. Sygnum (Switzerland), AMINA Bank (Switzerland, formerly SEBA), and Anchorage Digital (US, OCC-chartered) define this tier.

Category 2: Retail crypto-friendly neobanks

Mainstream consumer neobanks that added crypto trading and storage as a feature. Revolut, Cash App, Robinhood, N26 (limited markets), and SoFi sit here. Crypto is one product line among many. These are not crypto banks in a strict sense, but they are how most retail users access crypto inside a banking-style interface.

Category 3: Pure crypto neobanks

Digital banks where crypto is core, not a feature. Users get a debit card, fiat on and off ramps, and a unified balance of fiat and digital assets. Juno, Bleap, and a new generation of European and LATAM players target this space. The pitch is a bank designed for someone who already lives in crypto.

Category 4: Stablecoin and tokenized-deposit banks

The emerging frontier. Banks built around stablecoin rails, tokenized deposits, or on-chain settlement as the primary payment layer. Karsa for emerging markets, Mode for Web3-native treasury, and the tokenized-deposit experiments from JPMorgan (Kinexys), BNY Mellon, and Société Générale signal where the category is heading. For users this looks like a bank account; under the hood, money moves on public or permissioned blockchains.

The leading crypto banks in 2026

Sygnum Bank

Type: Institutional crypto bank, Switzerland and Singapore.

What they offer: Custody, trading, lending, tokenization, structured products. Banking license in Switzerland; capital markets license in Singapore.

Best for: Institutions, family offices, high-net-worth individuals needing fully regulated digital asset banking.

Marketing lesson: Sygnum built credibility through institutional PR, regulatory transparency, and named partnerships (PostFinance, SBI). Their playbook is the opposite of viral neobanks - slow, trust-led, B2B2C.

Anchorage Digital

Type: Federally chartered crypto bank, United States.

What they offer: Qualified custody, settlement, staking, governance, lending for institutions.

Best for: US institutions requiring OCC oversight.

Marketing lesson: Anchorage owns the phrase "federally chartered crypto bank" in US institutional conversations. The marketing wedge is regulatory positioning. The takeaway for any crypto bank: pick a defensible claim that competitors cannot copy, then repeat it everywhere.

AMINA Bank (formerly SEBA)

Type: Swiss crypto bank with Abu Dhabi and Hong Kong presence.

What they offer: Custody, trading, asset management, and structured products for institutions and qualified investors.

Best for: Global institutional clients needing multi-jurisdictional digital asset banking.

Marketing lesson: The 2024 rebrand from SEBA to AMINA is a case study in how regulated brands navigate identity changes without losing trust. The rollout led with regulatory continuity messaging before any product story.

Revolut

Type: Retail neobank with deep crypto integration.

What they offer: Multi-currency accounts, crypto trading on 100+ assets, staking, cards, and a full retail banking suite.

Best for: Mainstream users who want one app for fiat, FX, and crypto.

Marketing lesson: Revolut's crypto positioning is intentionally non-crypto-native. The product is sold as a banking feature, not a Web3 experience. This widened the funnel and is the single largest reason Revolut now serves more crypto holders than most pure crypto exchanges in Europe.

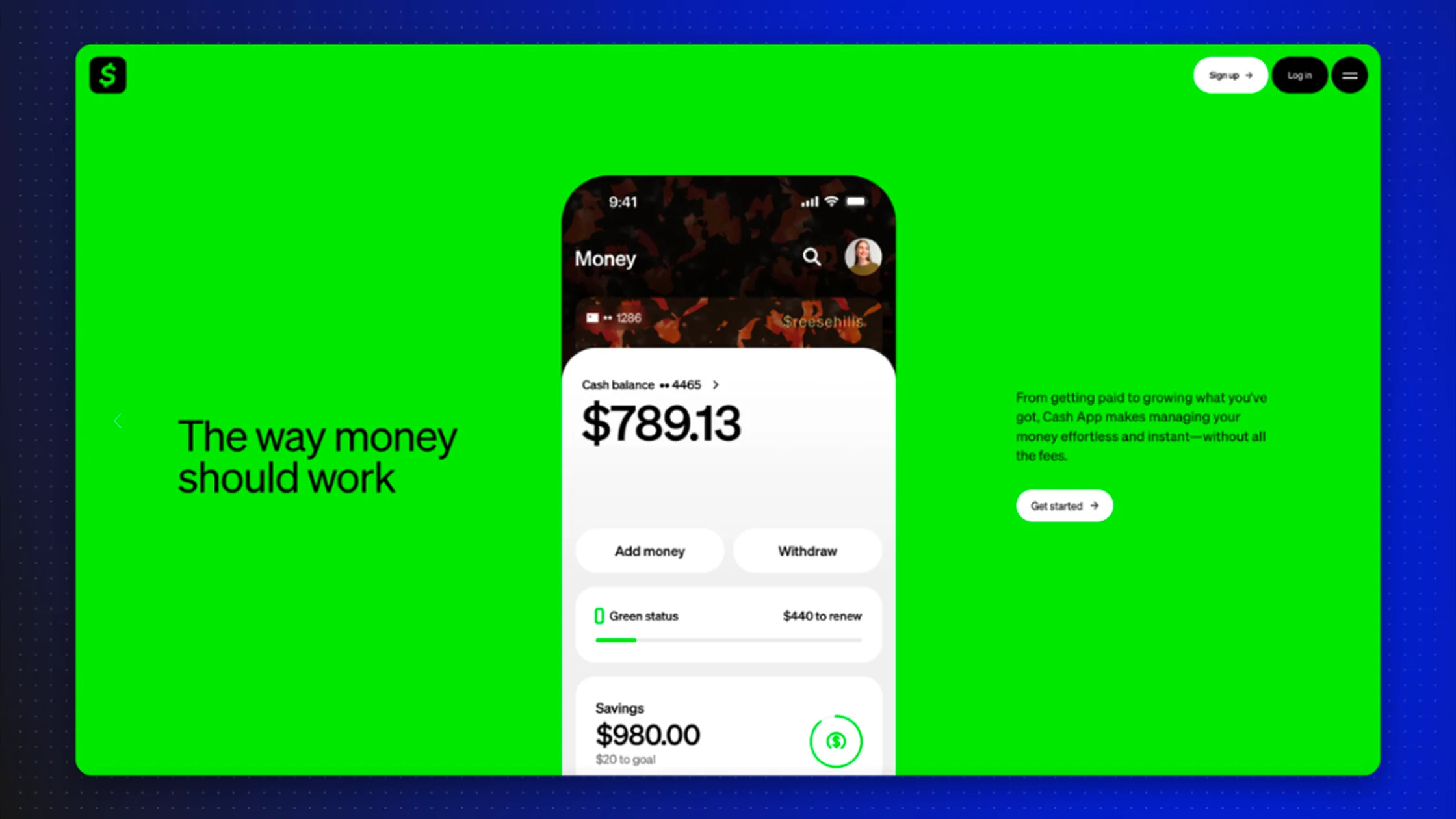

Cash App

Type: US peer-to-peer payments app with bitcoin and stocks.

What they offer: Bitcoin buying, holding, Lightning withdrawals, plus retail banking.

Best for: US users who want simple bitcoin exposure inside a payments app.

Marketing lesson: Cash App's Lightning integration earned bitcoin-native trust without alienating mainstream users. They picked one crypto asset, did it well, and let community advocacy do the marketing.

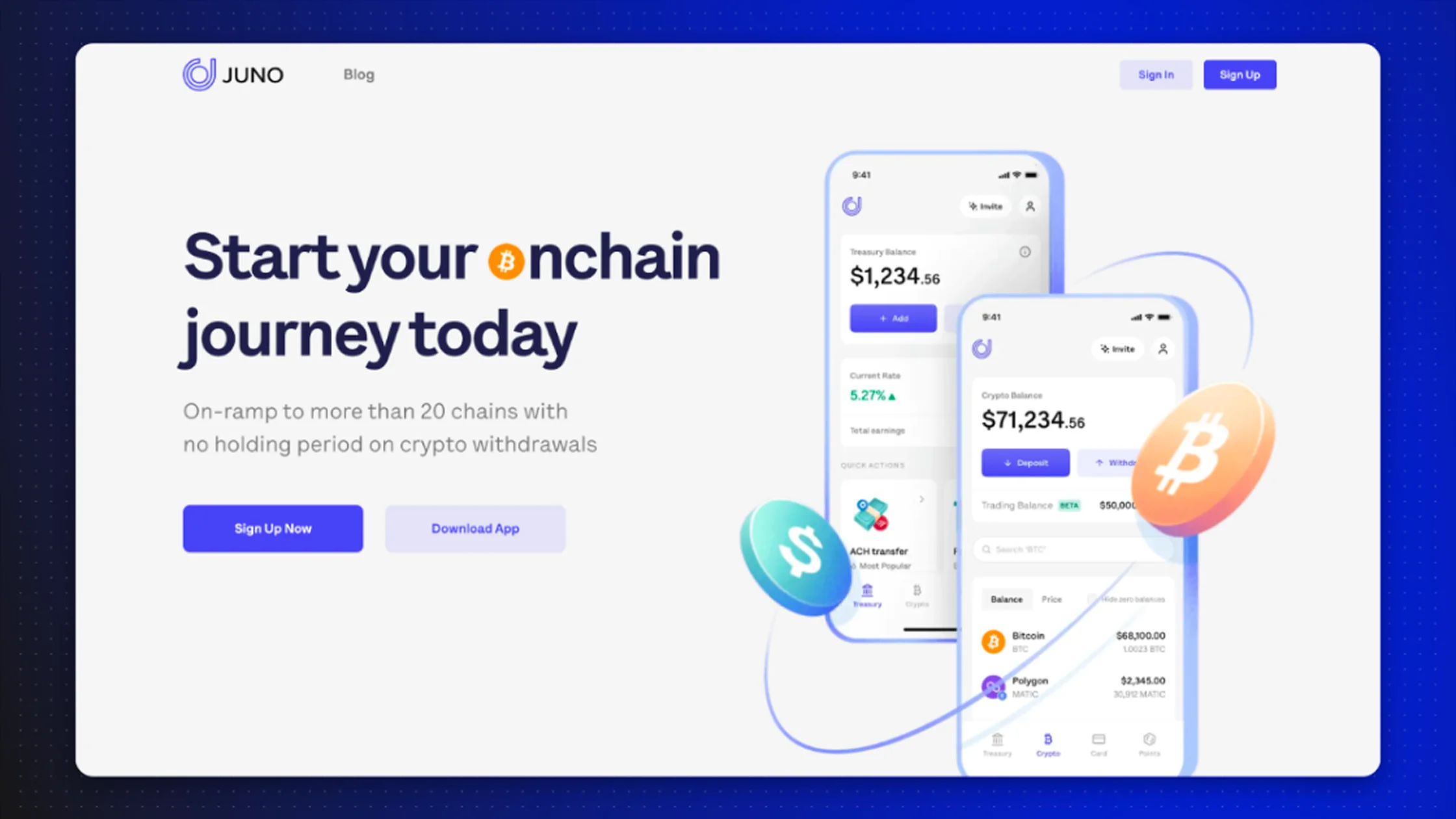

Juno

Type: US crypto-friendly neobank.

What they offer: USDC and stablecoin payouts, crypto debit card, banking account with high-yield options.

Best for: Crypto-native users wanting a US bank account that natively handles stablecoins.

Marketing lesson: Juno's positioning around "get paid in crypto" speaks directly to a defined user (remote workers, crypto employees) and avoids the broad-target trap.

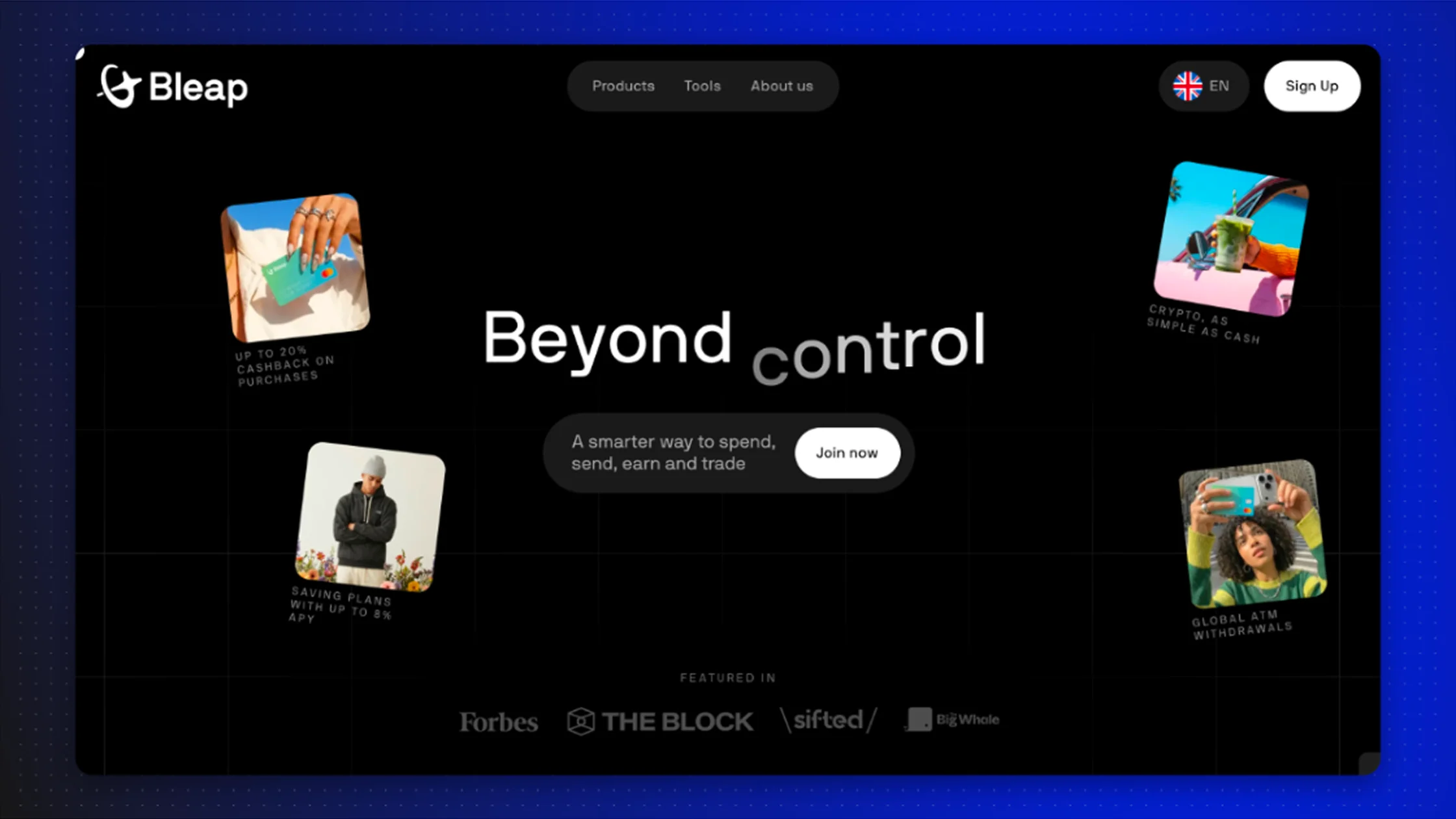

Bleap

Type: European Web3 banking app.

What they offer: Self-custody wallet plus card and IBAN; spend stablecoins like fiat.

Best for: European crypto users who want self-custody and traditional payment rails together.

Marketing lesson: Bleap leads with self-custody as the positioning differentiator. The pitch is a Web3 wallet with bank-grade UX, not a bank with a Web3 feature.

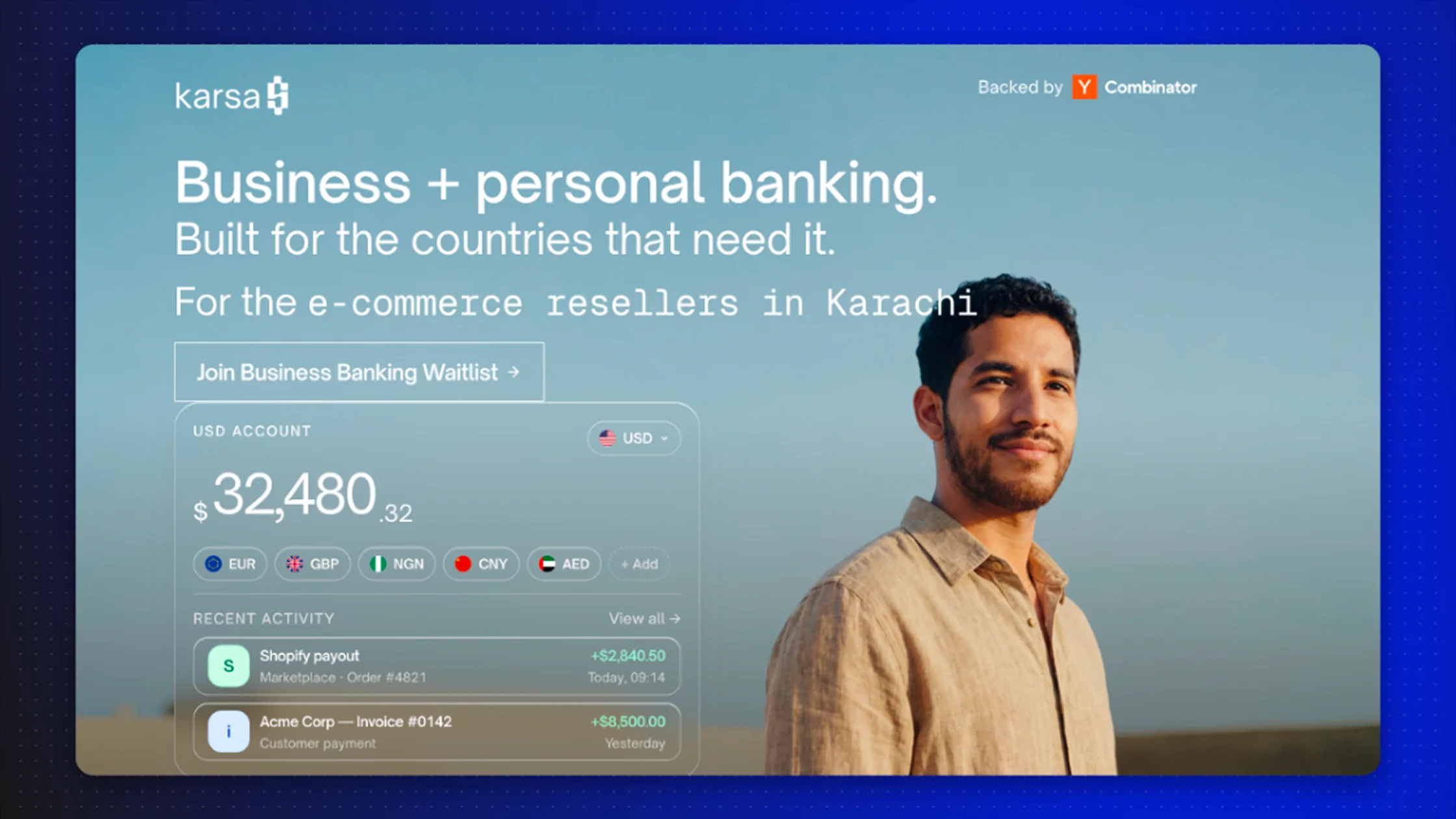

Karsa

Type: Stablecoin neobank, emerging markets focus.

What they offer: Dollar-stablecoin accounts, payments, savings, and remittance for emerging-market users.

Best for: Users in inflationary economies wanting USD exposure through stablecoins.

Marketing lesson: Karsa's narrative - banking for the next billion through stablecoins - is precisely the kind of positioning that earns category ownership before mass adoption arrives.

How to choose a crypto bank: 7 buyer criteria

1. Regulatory protection

Check for a banking license, FDIC or SIPC equivalent insurance, and the jurisdiction of incorporation. Custody arrangements matter as much as the brand name on the door.

2. Asset and chain coverage

Which cryptocurrencies and stablecoins are supported? Which chains? Whether withdrawals are allowed to an external wallet? Сustodial-only platforms lock users in.

3. Fiat rails

SEPA, SWIFT, ACH, FedNow, Faster Payments. The fiat side is often where pure crypto banks fall short. A crypto bank without strong fiat rails is an exchange in disguise.

4. Card and spending

Visa or Mastercard, fees, reward structures, geographic acceptance, and whether spending pulls directly from crypto or auto-converts. Cards are the moment crypto becomes useful in daily life.

5. Yield and earn

Stablecoin yield, staking, and savings products. Sustainable yield versus subsidized yield. Disclosure of underlying strategies.

6. Fees and FX

Conversion spreads, withdrawal fees, monthly account fees, and ATM fees. Many crypto banks hide costs in spreads.

7. Compliance and KYC posture

Onboarding speed, document requirements, and ongoing transaction-monitoring posture. A bank that loses customers at KYC is not a real bank.

What crypto bank founders can learn from the leaders

Five patterns repeat across the winning crypto banks of 2024-2026:

- Pick one positioning wedge and repeat it. Anchorage owns "federally chartered." Sygnum owns "fully regulated Swiss." Bleap owns "self-custody with a card." Karsa owns "stablecoin banking for emerging markets." Generic positioning loses to specific positioning every time.

- Community is the acquisition channel. Crypto users trust other crypto users. KOL programs, founder content on X, Discord and Telegram communities, and earned PR in crypto media compound into a defensible top-of-funnel.

- Regulation is a marketing asset. The leading institutional crypto banks turned compliance into copy. License numbers, audit reports, and named regulators feature on homepages. Retail neobanks should do the same.

- Stablecoins are the wedge into emerging markets. Karsa and similar players are showing that the next billion crypto users come through stablecoin banking, not through trading.

- Marketing must be Web3-fluent and finance-fluent at once. Pure Web3 marketing teams underdeliver on banking trust signals. Pure fintech marketing teams underdeliver on community velocity.

The 2026 outlook for crypto banking

Three shifts will define the next 24 months:

- Stablecoin neobanks will outgrow general crypto banks. The fastest-growing accounts in 2026 will be denominated in dollars but settled on-chain.

- Tokenized deposits will move from pilot to product. JPMorgan Kinexys, BNY, and Société Générale are early signals. Banks that wait will be outsold by banks that integrate tokenized rails.

- AI-led discovery will reshape acquisition. Users asking ChatGPT or Perplexity which crypto bank to use are already a meaningful share of demand. Crypto banks that show up in AI answers will compound faster than those relying on Google SERPs alone.

FAQ

What is the best crypto bank?

There is no single best crypto bank. The right answer depends on whether you are an institution (Sygnum, Anchorage, AMINA), a retail user wanting a familiar bank with crypto features (Revolut, Cash App), or a crypto-native user wanting stablecoin-first banking (Juno, Bleap, Karsa).

Is a crypto bank the same as a crypto exchange?

No. A crypto bank holds or partners with a banking license, offers fiat payment rails, and provides depositor protection on fiat balances. A crypto exchange is a trading venue. The line is blurring as exchanges add banking features and banks add trading, but the regulatory designation matters.

Are crypto banks safe?

Regulated crypto banks with banking licenses are subject to the same supervisory regimes as traditional banks for their fiat operations. Crypto custody arrangements vary. Always check who holds the digital assets, how, and under what regulatory regime.

What is a stablecoin neobank?

A stablecoin neobank is a digital bank where dollar-denominated stablecoins are the primary unit of account or payment rail. Users hold balances in stablecoins, transact globally with low friction, and access fiat conversion when needed. Karsa and Mode are leading examples; expect rapid growth in this category through 2026 and 2027.

Which crypto banks are best for institutions?

Sygnum Bank, AMINA Bank, Anchorage Digital, BitGo, and Komainu lead institutional crypto banking. The decision typically comes down to jurisdiction (Switzerland, US, Singapore), custody architecture, and the depth of prime services offered.

How do crypto banks make money?

Crypto banks earn through trading spreads, custody fees, interchange on card transactions, FX margins, lending against crypto collateral, staking commission, and increasingly through tokenized deposit and on-chain settlement fees.

Working with Lunar Strategy

Lunar Strategy has built marketing engines for 250+ crypto and Web3 projects since 2019, including Polkadot, ICP, and OKX. Our team brings the Web3-native acquisition capabilities - KOL and influencer networks, community infrastructure, crypto-native PR, crypto social media marketing, and end-to-end go-to-market strategy - that the new generation of crypto neobanks, stablecoin banks, and Web3-native banking products need to scale.

If you are launching or scaling a crypto neobank or Web3-native banking product, book a free consultation with our team.

Explore all Lunar services or browse our case studies.